U.S. Export Statistics

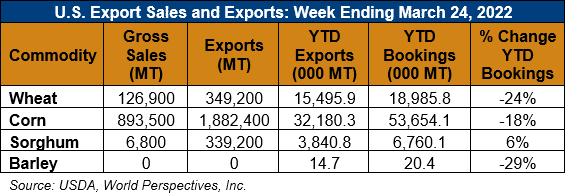

Corn: Net sales of 636,900 MT for 2021/2022 were down 35 percent from the previous week and 53 percent from the prior 4-week average. Increases primarily for Japan (217,800 MT, including 125,000 MT switched from unknown destinations and decreases of 7,600 MT), Colombia (103,800 MT, including 41,000 MT switched from unknown destinations and decreases of 20,100 MT), Mexico (86,600 MT, including decreases of 116,600 MT), Vietnam (69,300 MT, including 68,000 MT switched from unknown destinations), and Taiwan (66,000 MT switched from unknown destinations), were offset by reductions primarily for unknown destinations (74,300 MT), Lebanon (50,000 MT), and China (18,400 MT). Net sales of 286,800 MT for 2022/2023 were reported for unknown destinations (254,800 MT), Mexico (30,000 MT), and Honduras (2,000 MT).

Exports of 1,882,400 MT were up 26 percent from the previous week and 24 percent from the prior 4-week average. The destinations were primarily to China (457,600 MT), Japan (432,200 MT), Mexico (335,200 MT), Colombia (170,800 MT), and Canada (96,800 MT).

Optional Origin Sales: For 2021/2022, new optional origin sales of 60,000 MT were reported for unknown destinations. Options were exercised to export 65,000 MT to unknown destinations from the United States. The current outstanding balance of 530,800 MT is for unknown destinations (300,000 MT), South Korea (130,000 MT), Morocco (60,000 MT), Italy (31,800 MT), and Saudi Arabia (9,000 MT). For 2022/2023, the current outstanding balance of 3,900 MT is for Italy.

Export Adjustments: Accumulated exports of corn to Mexico were adjusted down 698 MT for week ending March 17th. This shipment was reported in error.

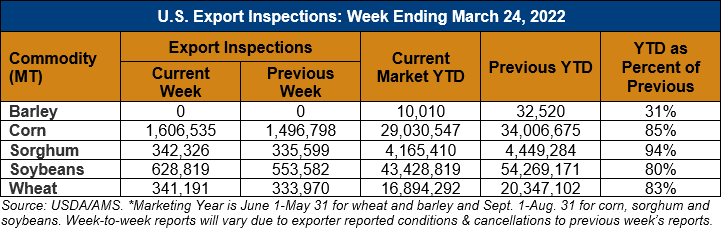

Barley: Total net sales reductions of 8,200 MT for 2021/2022 were up noticeably from the previous week and from the prior 4-week average. The destination was Japan. Total net sales of 8,200 MT for 2022/2023 were for Japan. No exports were reported for the week.

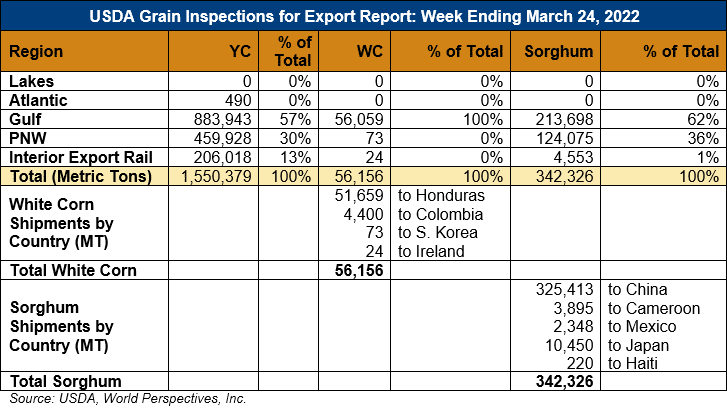

Sorghum: Net sales reductions of 16,200 MT for 2021/2022–a marketing-year low–were up noticeably from the previous week, but down noticeably from the prior 4-week average. Increases reported for China (50,800 MT, including 68,000 MT switched from unknown destinations and decreases of 23,000 MT) and Japan (1,000 MT), were more than offset by reductions for unknown destinations (68,000 MT). Exports of 339,200 MT–a marketing-year high–were up 33 percent from the previous week and 58 percent from the prior 4-week average. The destinations were primarily to China (328,300 MT) and Japan (10,500 MT).