Chicago Board of Trade Market News

Outlook

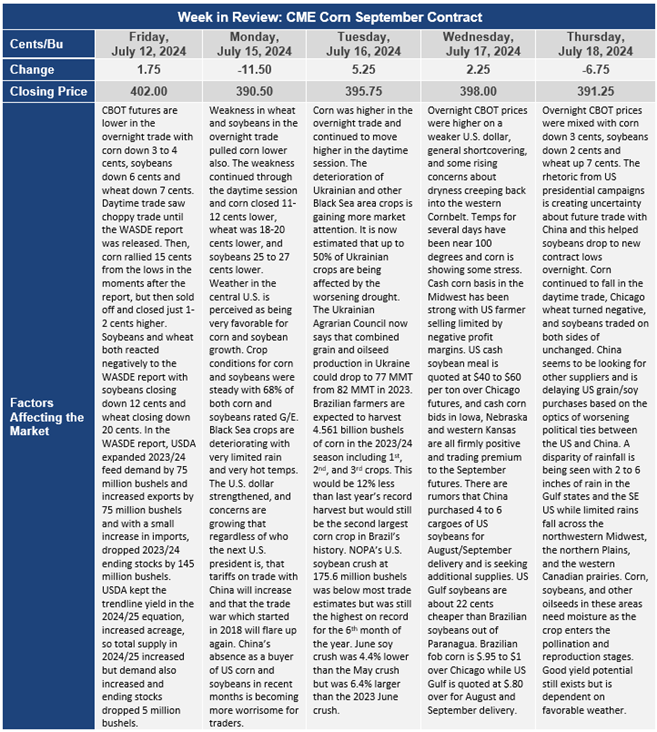

USDA’s July WASDE update surprised the market with stronger domestic feed demand and increased corn export demand in the 2023/24 marketing year. USDA increased both of these use categories by 75 million bushels, but raised imports by 5 million bushels, with the results being a 145 million bushel drop in 2023/24 ending stocks. Currently, U.S. export sales to date were only 15 million bushels from USDA’s sales expectations for the year and with strong Mexican corn train demand continuing, this likely prompted the increase in the export estimates. On the domestic demand front, U.S. cattle on feed numbers and substantial hog feeding numbers are being supportive to corn basis levels in the western cornbelt and indicate that feed usage is increasing.

The smaller U.S. carryover stocks mostly offset the increase in 2024/25 production as USDA kept the 181 bu/acre trendline yield and upped the harvested acres with the input from the June planted acreage report. (Note: with significant flooding in parts of southeastern South Dakota, northwest Iowa, southern Minnesota, and in both the Mississippi and Missouri River basins, it is likely that harvested acreage will be reduced by several million acres in either the September or October WASDE reports.)

New crop corn demand (2024/25 marketing year) was increased by USDA. They added 75 million in feed demand and 25 million in export demand. Instead of the trade’s expected 210 million bushel increase in 2024/25 ending stocks, ending stocks for 2024/25 dropped by 5 million bushels to 2.097 billion bushels.

The stronger old-crop demand outlook for U.S. corn crop comes at the same time as USDA sliced another 1 mmt from Argentina’s corn crop. This reduced the World Board’s 2023/24 world stocks by 3.26 mmt for October 2024.

The World Board only sliced 5 million bushels from beans’ old-crop imports and dipped its 2024 U.S. soybean output by 15 million bushels. These were the only two changes in soybeans’ old & new crop balance sheets. Overall, this reduced new-crop soybeans stocks by 20 million to 435 million bushels, but this carryover outlook remains large versus recent years. On the world level, the USDA sliced 500,000 metric tons from Argentina’s soybean crop to 49.5 mmt, but they left their Brazilian output unchanged at 153 mmt despite the heavy flooding that occurred in RGDS early this year. Prices for soybeans and soybean meal were lower in response to the report and continued to drop in the following days.

Brazil’s Conab raised the 2nd crop corn output by 1.8 mmt this month bumping up their overall output idea to 115.9 mmt. Conab left their 2024 soybean estimate at 147.4 mmt this month, but the USDA didn’t change their current 122 mmt & 153 mmt estimates so a significant gap still remains between the two estimated levels. There might not be much change in these numbers in the next few weeks, but there still remains plenty of uncertainty in U.S. crops as corn is about 50% done with pollination and soybeans beginning flowering. The next 5-6 weeks are highly important.

With the USDA’s 52 and 181 bu yields substantially higher than last year’s 50.6 and 177.3 yields, 2024’s U.S. production remains vulnerable for reduction. Last year’s U.S. dryness in May and June prompted the dip in their yields from initial May levels. This wasn’t expected this year, but the current yield ideas remain optimistic. However, a 1 bu/ac U.S. bean yield decline could reduce soybeans ending stocks by 85 million bushels to 350 million, the same as this year. A 2-3 bu/ac lower yield U.S. corn output would shave 170 to 250 million from the current 2.1 billion bushel ending stocks.