Chicago Board of Trade Market News

Outlook

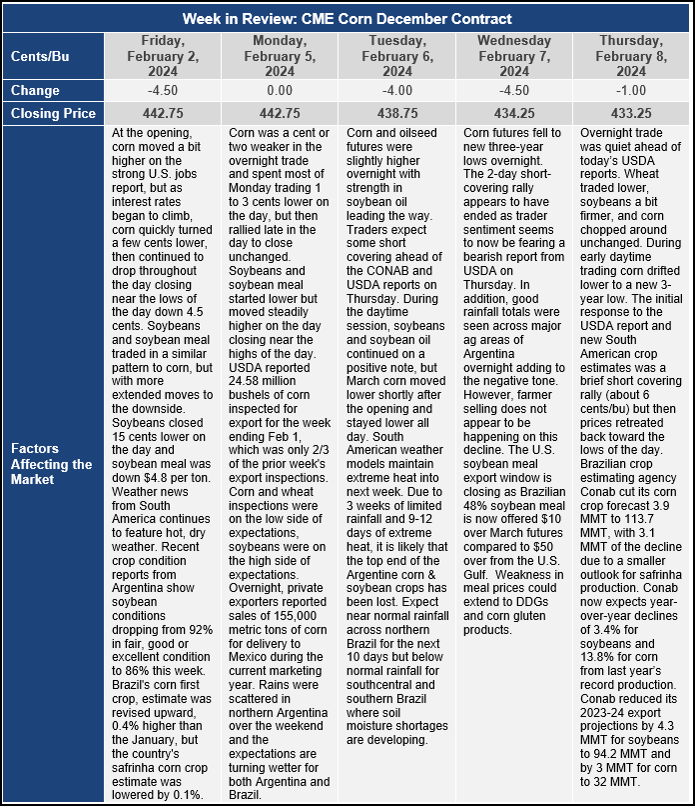

Chicago-traded corn and soybeans have begun February with a similar energy as last month, downtrends intact and making new lows. Corn fell nearly 5% last month, the most for January since 2015, which featured a similar fundamental situation for U.S. corn as this year. March corn continues to hover near three-year lows. Thursday’s poor export news for U.S. beans validates recent demand concerns from top buyer China, where the broader economy is still struggling to regain momentum post-COVID. This could continue pressuring nearby corn and particularly soybean futures.

New-crop futures will come under scrutiny this month, too, as the average price of November soybeans and December corn during February sets insurance guarantees to U.S. farmers for the 2024 growing season. These can impact planting decisions. Versus the February 2023 monthly averages, prices on February 1 were 19% lower for corn and 14% lower for soybeans. November soybeans are trading at about 2.47 times the value of December corn, not distinctly in favor of either crop as this inter-commodity dynamic can be just as important as the actual prices.

Karen Braun, a market analyst for Reuters, notes that the January price weakness does not have to continue in February for beans. Since 2010, March soybeans declined throughout January five other times aside from this year, and the contract notched gains in February all five times. The trend for corn is more mixed with five other losing Januarys since 2009, though futures moved even lower in February in two of those years, 2009 and 2020. Global economic turmoil is the common link between those two years.

Braun goes on to note that U.S. corn ending stocks for 2023-24 are estimated to be up 59% on the year, and 2015 is the most similar year as stocks as of January 2015 were seen rising 52% on the year. In January 2015, March corn futures were trading at the lowest levels for that time of year in five years, and today they are the lowest seasonally in four years. The old-new-crop futures curve is almost identical to 2015, with March trading nearly 32 cents per bushel under the December contract, suggesting relatively comfortable supplies in the immediate term.

Speculative positioning sets 2024 apart from 2015 and most other years, and it makes a potential argument for some price strength in February. Funds are holding record short positions for the early February time period, and this could lead to a significant rally when they begin to reduce their positions.

USDA’s February WASDE report for 2023/24 U.S. corn outlook is for lower food, seed, and industrial use and larger ending stocks. Corn used for glucose and dextrose is reduced 10 million bushels based on indicated usage to date. With no other use changes, U.S. corn ending stocks are up 10 million bushels from last month. The season-average corn price received by producers is unchanged at $4.80 per bushel.

Global coarse grain production for 2023/24 is forecast 3.8 million tons lower to 1,510.1 million. Foreign corn production is down, with reductions for Brazil, Mexico, and Serbia partially offset by increases for India and Turkey. Major global trade changes for 2023/24 include higher projected corn exports for Ukraine and Pakistan with reductions for Brazil, India, and Serbia. Barley exports are raised for Australia and Ukraine but lowered for Canada. Foreign corn ending stocks are down relative to last month.