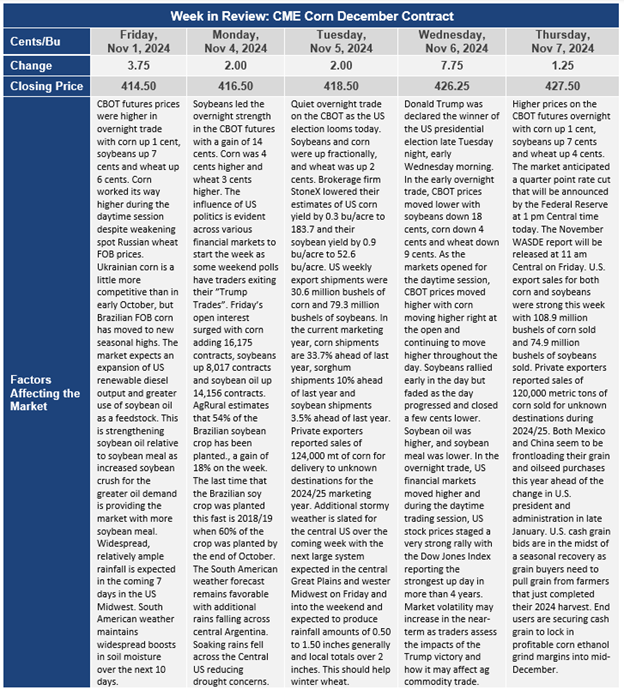

Chicago Board of Trade Market News

Outlook

USDA’s corn and soybean crop estimates aren’t likely to change much in Friday’s Crop Production Report. Barring any supply-side surprises, adjustments to usage forecasts will impact changes to 2024-25 ending stocks. USDA’s global wheat production forecasts might draw the most attention given declining private crop forecasts for several countries.

Early trade estimates are for corn production to drop by 15 – 25 million bushels, although the range from analysts is for a drop of 125 million bushels to an increase of 100 million bushels. U.S. corn ending stocks are expected to drop by 50 million bushels, but with the range of analysts expectations of down 175 million bushels to an increase of 70 million bushels.

The early soybean estimates are for production to be the same as the October estimate, at 4.557 billion bushels, although the range in analyst estimates ranges from 4.495 billion bushels to 4.640 billion bushels. Soybean ending stocks for the 2024/25 marketing year are expected to decline by an average of 18 million bushels, falling to 532 million bushels. The range of analyst estimates is for ending stocks of 475 million bushels to 585 million bushels.

Expectations for global corn carryover is a decline to 305.7 mmt from 306.52 mmt in the October report. Global soybean ending stocks are expected to decline by 0.6 mmt, falling to 134.06 mmt compared to 134.65 mmt in the October report.

World wheat ending stocks for 2024/25 are expected to decline by 0.93 mmt in the November report with ending stocks for 2024/25 at 256.79 mmt versus 257.72 mmt in the October report.

The U.S. corn and soybean harvest is nearly complete. U.S. producers have harvested more than 94% of soybeans and 91% of corn. Generally wet weather across much of the Midwest in the past week has delayed the finish of harvest for a few days but has been very welcome for the winter wheat crop, pastures, and for cover crops that have been planted following corn and soybean harvest. Corn harvest is 16 points ahead of the 5-year average. Soybean harvest is nearly done except for North Carolina which is at 43% harvested versus 44% normally.

The U.S. Federal Reserve Bank cut short-term interest rates by another quarter point at their meeting on Thursday. Real U.S. GDP grew at a 2.8% rate during the summer months and with inflation near the Fed’s target of 2%, the combination should support continued economic growth. Some macro market concerns are the potential continuation of deficit spending by the U.S. government. President-elect Trump has outlined some potential tax cuts and other programs that could keep the U.S. government running a budgetary deficit. The sustainability of continued growth and low inflation relies on sound fiscal policy and economic adjustments moving forward.

The Standing Committee of China’s legislature began an important five-day session in Beijing, where economic stimulus measures are set to be discussed. The measures approved during this meeting are expected to signal the leadership’s approach to handling the country’s economic challenges.