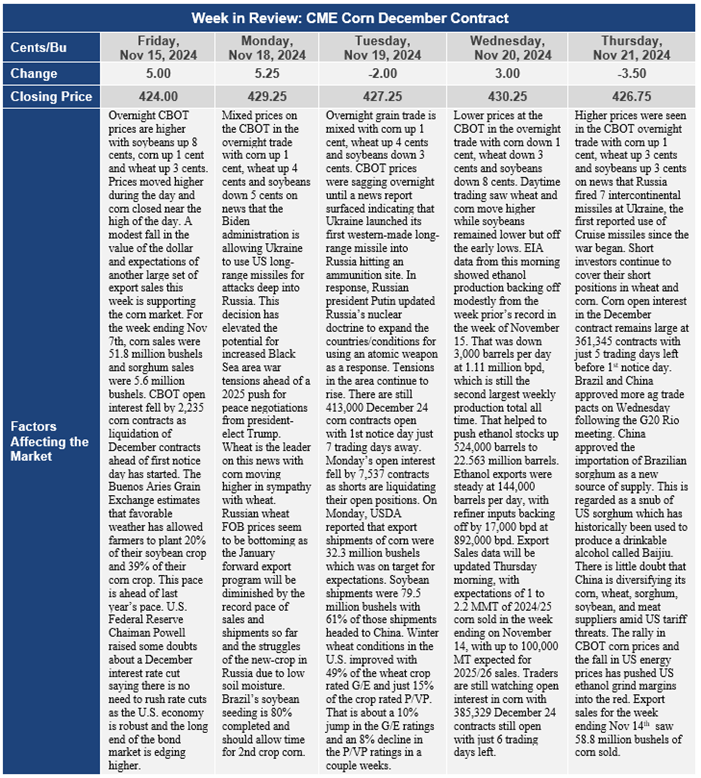

Chicago Board of Trade Market News

Outlook

In the U.S., corn harvest is basically completed. USDA dropped reporting on weekly harvest progress which usually indicates that harvest is 99% or more complete. Likewise, soybean harvest is basically completed also. With carryover stocks and production from 2024, the U.S. will have nearly 17 billion bushels of corn available during the 2024/25 marketing year. Domestic feeding will account for 5.825 billion bushels and ethanol production will use at least 5.45 billion bushels with the potential for increases in the amount processed for ethanol to increase if the U.S. economy remains strong and ethanol exports remain strong. The Energy Information Administration (EIA) reports that U.S. fuel exporters are on track to export a record amount of ethanol in 2024. The increase in exports this year has largely been driven by demand in countries with biofuel blending requirements and U.S. ethanol prices that make U.S. ethanol very competitive in world markets. U.S. corn exports are expected to increase in the 2024/25 marketing year compared to the prior year. Current expectations are for exports of 2.325 billion bushels of corn, up 1.4% from the 2023/24 marketing year.

World coarse grain production is expected to be 1,499.7 mmt, down from 1,504.6 mmt in 2023/24. As world production estimates get updated, the quantities expected to be produced have been slowly reduced. Total world supply of coarse grains is expected to be 1,844.3 mmt, up 3.4 mmt from a year ago based on larger beginning stocks for 2024/25 than existed in 2023/24. World trade in coarse grains is expected to slow during the 2024/25 marketing year, dropping by 10.5 mmt compared to the 2023/24 marketing year. This will be a 4.3% reduction in global coarse grain trade. Despite this drop in global coarse grain trade, total use of coarse grains on a global basis is expected to increase by 17.8 mmt, a 1.25 increase in total use. World ending stocks for coarse grains for 2024/25 are expected to decline from 344.3 mmt to 329.8 mmt, a 4.2% decline.

In a few weeks, South American weather will begin to have a more direct impact on crop potential. So far, the primary concern has been getting the crops planted in Argentina and the soybean crop planted in Brazil. Argentina’s corn planting progress is estimated to be about 50% done and unlike some recent years, there’s been no need to wait for moisture-replenishing rainfall before planting. This means that it is likely that a greater share of Argentina’s arable land will be dedicated to early-planted corn. It is likely that 60% of Argentina’s corn crop will be planted by December 1st which compares to just 25% both last year and the year before. More corn will pollinate in December as 20% of Argentina’s corn crop was planted prior to October 10th and this implies that a greater share of Argentine corn will be harvested in March and April rather than June. This is much different than in recent years.

In general, rainfall of 4 inches in December in Argentina sets the stage for an above-trend yield. Rainfall of 3 inches has a mixed correlation and places a heavier reliance on cooler than normal temperatures as well as February and March rainfall. Rainfall of less than 2 inches in Argentina in December essentially guarantees a below-trendline Argentine corn yield. December climate guidance favors Argentina’s “ag belt” and the medium-term confidence is high with respect to the return of rain to this area which accounts for 75% of Argentina’s corn production. South American weather, on a daily basis, will likely become a greater influence on daily and weekly price discovery beyond the next two weeks.