Chicago Board of Trade Market News

Outlook

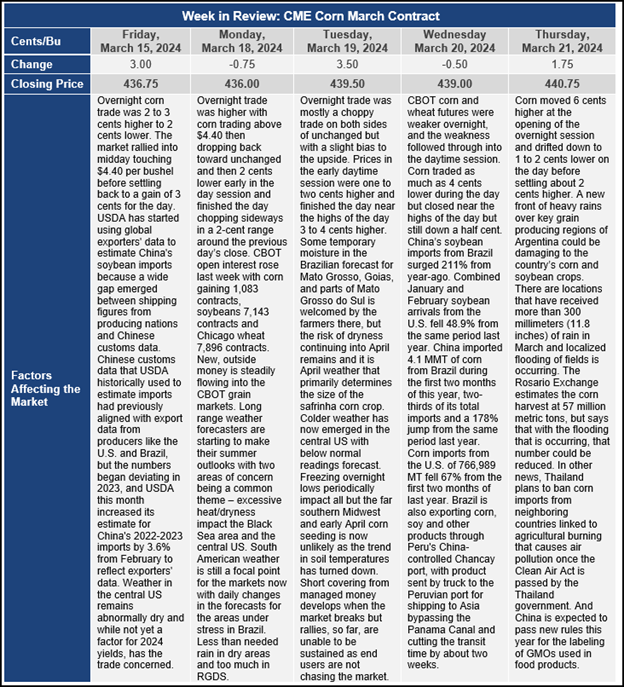

Bottoming action continues to be seen as CBOT futures chop sideways to higher this week. The downtrend that has been in place since October 2023 currently provides upside resistance in the May corn contract between $4.45 and $4.50 per bushel. If the market can work its way through that resistance, then an intermediate uptrend could be developing that could support the market moving initially to the $4.60 level and eventually up towards strong resistance between $4.85 and $5.05 basis the May contract. It appears that the market pierced through the trendline to the upside in Thursday’s trade.

It is reported that the EU is preparing to place import duties on Russian grain imports as a way to stem the protests from its farmers. The proposed duty would be either $95 or $104 euros per metric ton. Currently, only modest amounts of Russian grain are imported into the EU. It is Ukrainian grain that is the focus of the protests, and it is doubtful that the leadership in Brussels will place similar duties on Ukrainian grain imports. The EU farmer protests are unlikely to relent until there is a duty mechanism to slow the flow of grain from Ukraine.

China has approved another 27 GMO seed traits for planting in the future. These approvals will not impact 2024 GMO seed availability as China tries to boost domestic corn and soybean yield through seed technology. It is likely that it will take years for Chinese farmers to fully adopt the new seed and any impacts on production in the near future will be modest.

The Federal Reserve kept interest rates at a range of 5.25% to 5.50% following its two-day monetary policy meeting. The Fed’s dot plot showed a growing number of officials are coalescing around the view rates would end 2024 at 4.50% to 4.75%, equivalent to three 25 basis point cuts. The projections now signal core inflation will end the year higher and unemployment slightly lower than predicted in December. Officials upgraded the gross domestic product projections for 2024 to 2.1% expansion with inflation at 2.4% by the end of the year. The grain markets reacted positively to this news as it is seen as supportive to prices for assets and goods such as commodities.

In U.S. farm bill news, it now looks like the House may have a proposal to put on the table by late May and action on the proposal could happen in June. Key items for U.S. export markets are proposals for significant funding boosts for the Market Access Program (MAP) and Foreign Market Development Program (FMD), but back-loaded due to current Regional Agricultural Promotion Program (RAPP) funding. The U.S. ag sector is seeking over $900 million in aid to regain overseas markets lost to competitors like Brazil and Russia. USDA has received applications for more than three times the $300 million initially allocated in the first round of a five-year export promotion plan. The Regional Agricultural Promotion Program (RAPP), totaling $1.3 billion and announced last year, aims to assist the industry in accessing new markets for American crops. Funds from this program must be used to diversify markets, with a focus on expanding into Southeast Asia, the Middle East and Africa. The U.S. aims to capitalize on the growing middle class and increased buying power in these regions.