Chicago Board of Trade Market News

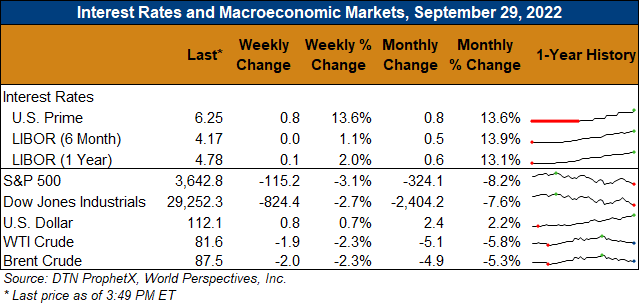

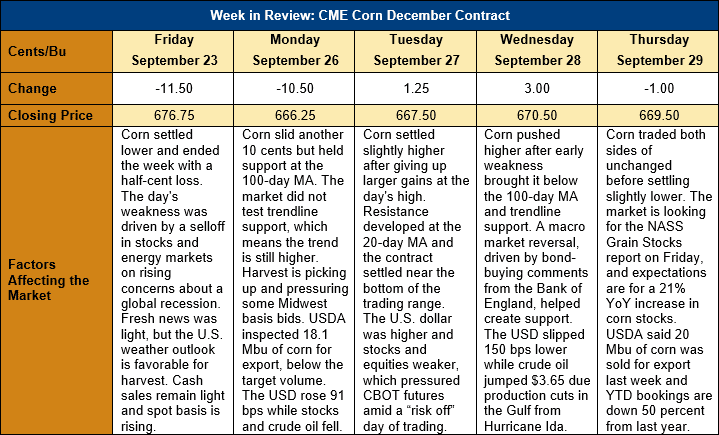

Outlook: December corn futures are 6 ¼ cents (1.1 percent) lower this week after a pronounced selloff in macroeconomic markets created spillover weakness in CBOT commodities. Concerns of a possible global recession amid high inflation rates and rising interest rates created “risk off” and liquidation trade in world equity, energy, and bond markets during the past week. That, combined with large currency fluctuations, kept corn futures in a defensive mode though signs of market strength are still evident.

The U.S. weather outlook remains favorable for the final stages of finishing the crop and the fall harvest. On Monday, USDA said 58 percent of U.S. corn is rated “mature” and harvest was completed across 12 percent of fields. Both figures are down slightly from their respective five-year averages but are not cause for concern. The outlook features above-normal temperatures and mostly dry conditions for the Corn Belt, which will help accelerate harvest. Early this week, overnight lows in parts of Minnesota and Iowa approached freezing, but no crop damage is expected this late in the growing season. The start of harvest is creating some basis weakness in isolated parts of the Midwest, but spot bids remain historically firm.

The USDA’s latest Export Sales report featured 0.599 MMT of gross export sales for corn and 0.574 MMT of corn exports, with the export figure rising 2 percent from last week. YTD corn exports total 1.601 MMT, up 5 percent from last year’s pace that was slowed by the impacts of Hurricane Ida. YTD bookings (exports plus unshipped sales) now total 12.995 MMT, down 49 percent from last year. YTD bookings currently account for 21.5 percent of USDA’s 2022/23 export forecast.

At Noon ET on Friday, 30 September 2022, USDA will release its quarterly Grain Stocks report. Analysts are expecting 37.975 MMT (1.495 billion bushels) of corn in storage to start the 2022/23 marketing year. If correct, that figure would be up 21 percent from last September. The report will largely define the 2021/22 ending stocks and, therefore, beginning stocks for the current marketing year. The report has historically offered surprises for the market and trade could be volatile following its release.

From a technical standpoint, December corn futures are drifting sideways and looking for solid technical support. This week’s macro-market weakness in currency fluctuations briefly caused December corn to below key support levels at the 100-day MA and a supporting trendline at $6.66 ¾ on Wednesday. The contract, however, rallied on a combination of end-user buying and short-covering and settled above both points by the day’s end. The latter fact points to underlying strength in the market and suggests the sideways trend will continue. Seasonally, corn prices often weaken during harvest before gradually trending higher through the winter and spring. This year, however, with tensions again rising in Ukraine, drought a growing issue for South America, and tight ending stocks predicted for the U.S. 2022/23 crop, harvest pressure will likely be minimal. Consequently, steady/higher trade seems the most likely outlook for CBOT corn futures.