Chicago Board of Trade Market News

Outlook

Uncertainty about the upcoming U.S. presidential election results is having some impacts on not only U.S. commodity markets but also world commodity markets. The political rhetoric includes threats of actions such as tariffs that could become disruptive to corn and soybean flows from the U.S. if countries affected were to take retaliatory actions. Campaign speeches appear to be prompting some importers to speed up the time frame for grain shipments and have U.S. grain merchandizers scrambling to ship out as much corn and soybeans from the record 2024 U.S. crop ahead of the presidential elections, and for sure, ahead of the inauguration of the next president in January. Nearly 2.5 mmt of U.S. soybeans were inspected for export last week, including 1.7 mmt bound for China. This is the highest level of weekly export inspections in the past year.

Nearly 1 mmt of corn were inspected for export last week also. This compares to 506.6 tmt last week and 472.4 tmt of corn exports in the corresponding week a year ago. To date in the current marketing year, corn export inspections are 5.79 mmt compared to 4.44 mmt a year earlier. That is a 30% increase. This “pull forward” of export shipments is likely to last at least through the election, which is in two weeks, and could extend into January if Donald Trump is elected president. If Kamala Harris wins the election, the rush to move exports before inauguration day in late January could ease up.

Chinese buyers of grain appear to be reluctant to book U.S. grains and oilseeds for shipments beyond January. Instead, these buyers are booking Brazilian soybeans and paying up to a 40-cent premium for those soybeans, compared to what they could book U.S. soybeans for that time period of delivery. At least one analyst believes this pull-forward and then fall-off in export shipments could result in U.S. soybean exports falling short of the latest USDA soybean export estimate.

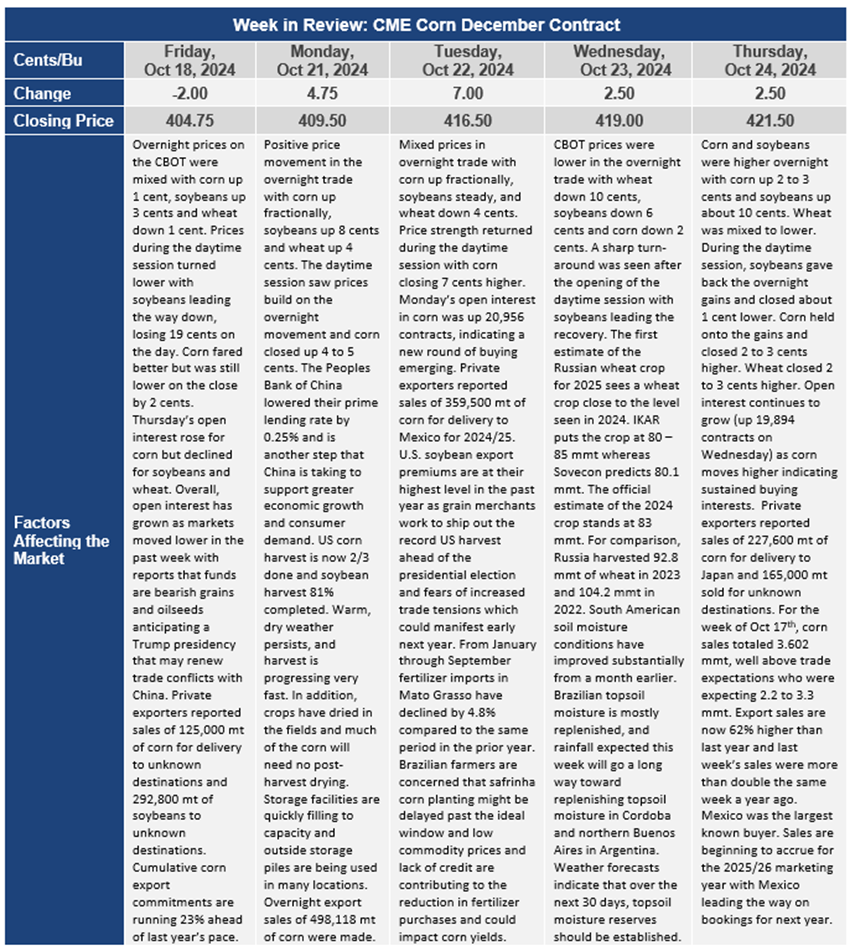

Current shipments of corn are also strong with Mexico being the number one destination of corn exports from the U.S. Earlier this week, private exporters reported 359 tmt of corn sold to Mexico for delivery in the 2024/25 marketing year and another 100 tmt to unknown destinations. And over the past week there were export sales of 169 tmt of corn to Mexico, 130 tmt to South Korea, and 198 tmt of corn to unknown destinations.

The International Monetary Fund (IMF) lowered their 2025 global GDP forecast amid what they deem to be increasing risks of slower economic growth. They cite geopolitical risk with increased potential of regional conflicts that could affect commodity markets. These risks include a rise in protectionism rhetoric, protectionist trade policies, and disruptions to trade directly resulting from some of the regional conflicts (ships being targeted in military actions, pirate attacks, etc.). The IMF’s forecast is for 3.2% global growth, down 0.1% from last year. U.S. economic growth was raised to 2.8%; Eurozone economic growth is forecast at 0.8% this year and 1.2% in 2025. Japan’s economy is forecast to slow to 0.3% growth this year but improve to 1.1% growth in 2025. China’s economy is expected to slow to 4.8% this year and further slow to 4.2% growth in 2025. India’s economy is expected to moderate from 8.2% growth in 2023 to 7% in 2024 and further moderate to 6.5% growth in 2025. Slower growth could keep commodity prices under pressure, at least in the near term.

The U.S. corn harvest was 65% complete at the end of last week and should be 80-85% complete by the end of October. Harvest pressure should abate in November and basis levels in the U.S. stabilize.