Chicago Board of Trade Market News

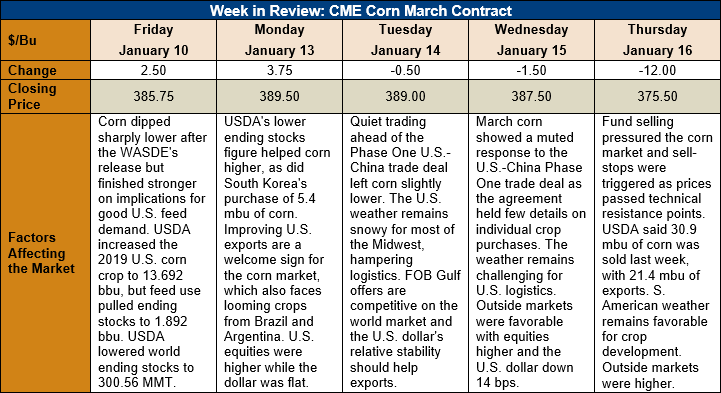

Outlook: March corn futures are 10.25 cents (2.7 percent) lower this week after two notably volatile trading days. Last Friday, USDA’s WASDE surprised traders from several directions, which left the futures market to trade lower before it finished the day up 2 ½ cents. Then, on Thursday, January 16, a pronounced selloff across the CBOT pulled March corn futures to 12-cent losses.

The surprises in last week’s WASDE started an increase to the 2019 U.S. corn yield, which is now estimated at 10.55 MT/ha (168 BPA), where the market had been projecting a decrease. USDA did note that it would resurvey parts of the Midwest hit hardest by the delayed harvest, though the resurvey is not expected to make a significant difference in final production figures. USDA estimated that the 2019 U.S. corn crop reached 347.795 MMT (13.692 million bushels).

The larger-than-expected yield was initially interpreted by the futures market as bearish, but the Grain Stocks report (released concurrently with the WASDE) data implied a much higher feed use during the September-November period. That was further reflected in the WASDE, where 2019/20 U.S. corn feed use was increased by 6.35 MMT (250 million bushels). That was the second major surprise for the day, and one that supported the futures market.

USDA made only minor changes to other parts of the U.S. corn balance sheet, but lowered ending stocks to 48.06 MMT (1.892 billion bushels). The agency’s data suggests a 13.4 percent ending stocks/use ratio, the lowest since the 2015/16 crop year. Despite the lower ending stocks estimate, USDA left its farm price forecast unchanged at $151.57/MT ($3.85/bushel).

Elsewhere in the WASDE, USDA increased world corn production by 2.2 MMT based on higher U.S., Russian, and European crop estimates. World feed use was revised higher by 7.6 MMT and total trade was lowered by 1 MMT. World corn ending stocks fell 2.8 MMT as a result of these adjustments, but 2019/20 ending stocks are projected at 297.8 MMT – slightly above analysts’ pre-report estimates.

The weekly Export Sales report showed gains in both sales and export figures. Corn net sales reached 784.8 TMT while exports grew 6 percent to 544.7 TMT. YTD exports stand at 9.4 MMT, down 55 percent while YTD bookings are 19.3 MMT, down 40 percent. For sorghum, the report noted net sales of 22.1 TMT and exports of 22.7 TMT. Barley net sales reached 800 MT and an equal volume was exported last week.

Cash corn prices are slightly firmer this week with the national average price reaching $146.87/MT. Basis has strengthened slightly under growing commercial demand and now averages 12 cents under March futures. Barge CIF NOLA prices are down 1 percent this week while FOB NOLA offers are 2 percent lower at $173.75/MT.

From a technical standpoint, March corn has broken out of its recent sideways trading pattern but found solid commercial support/buying activity as it neared $3.75/bushel. The recent selloff was precipitated by broader fund liquidation of agricultural holdings as well as an effort to extend corn short positions. As the futures market passed key technical points, sell-stops were triggered, which accelerated the selling. Futures spreads are tightening, however, and commercial buying was active on the break. Typically, those factors indicate long-term support for the market as well as likely price appreciation potential. While funds now hold a major short position in corn, they may have trouble keeping it with changes to global trade politics and smaller world ending stocks. Moreover, NOAA’s long-term forecast suggests the U.S. Midwest may face another challenging planting season, which would surely spark a market rally.