Distiller’s Dried Grains with Solubles (DDGS)

DDGS Comments: DDGS prices are higher this week as supplies tighten amid continued declines in ethanol run rates. Concurrently, rallies in feedstuffs markets, including physical corn priced at or above $8.00/bushel in parts of the Midwest, are offering support for DDGS values. The Kansas City soymeal/DDGS ratio is hit 0.6 this week, up from 0.58 last week and is above the three-year average of 0.48. The DDGS/cash corn is steady with last week at 1.04 but below the three-year average of 1.06.

U.S. railroads are experiencing a shortage of railcars that has started to impact the ethanol industry, among others. Merchandisers indicate the issue is unlikely to cause significant problems for the DDGS market because “DDGS can usually be moved at only a slight discount [to railcars] in trucks.” Ethanol plants “can still stay profitable by shipping DDGS into truck markets”, according to industry sources. Rail rates for routes in this report are up $10-12/MT, on average, compared to last week.

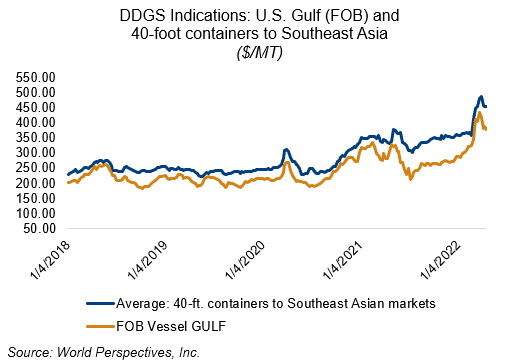

Barge CIF NOLA and FOB Gulf DDGS values are lower this week with barge rates falling $16-20/MT while FOB Gulf offers are down $10/MT. Spot FOB Gulf offers are averaging $379/MT this week.

Prices for containerized DDGS into southeast Asia are steady for the second time in as many weeks. Changes in ocean freight rates have been muted this week, which has kept some stability in containerize export markets. Offers for 40-foot containers to Southeast Asia are up $1/MT this week at $459 for May/June shipment.