Ethanol, Fuels and Co-Product Pricing

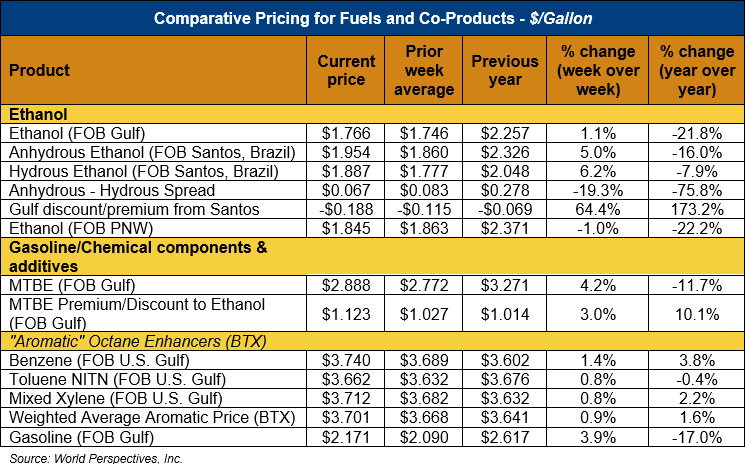

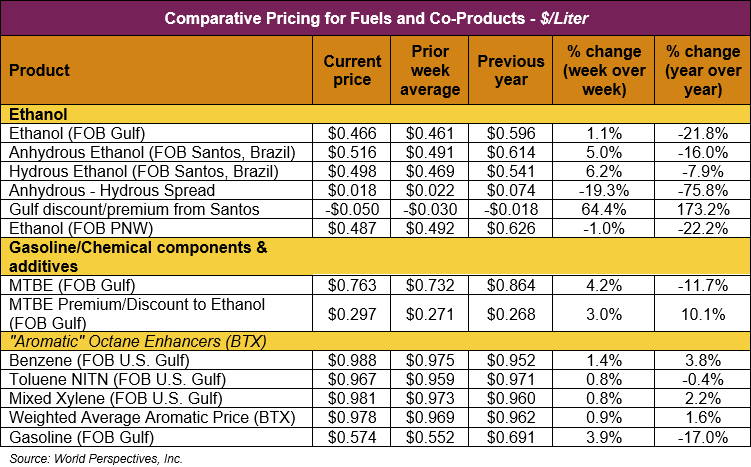

Market Outlook: U.S. ethanol prices ended last week unchanged but rallied in early week trading and rose 2.5 percent through Tuesday’s close. Midwest wholesale rack ethanol prices were lower to end last week but were up 1.5 percent through Tuesday’s market close to their last quote of 46.97 cents/liter (177.79 cents/gallon).

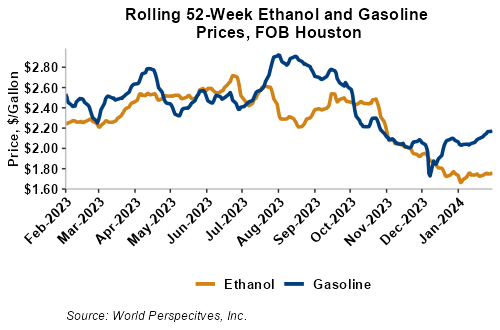

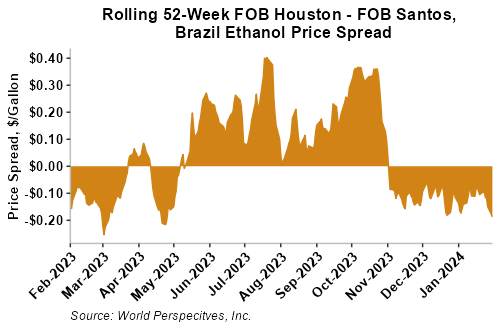

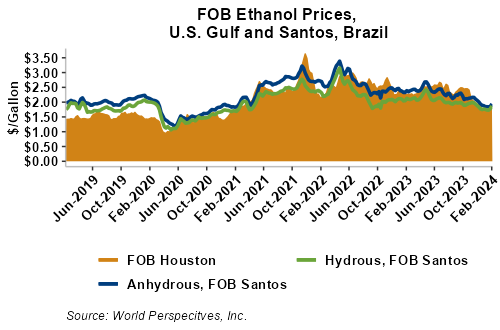

FOB Houston ethanol prices finished last week 1.3 percent higher and are up 1.1 percent through Tuesday’s trading from Friday’s close. FOB Houston ethanol prices are quoted at 46.64 cents/liter (176.56 cents/gallon). FOB Santos, Brazil anhydrous ethanol prices were higher last week; they are up in early week trading, rising 5 percent to 51.62 cents/liter (195.405 cents/gallon) through Tuesday’s trading.

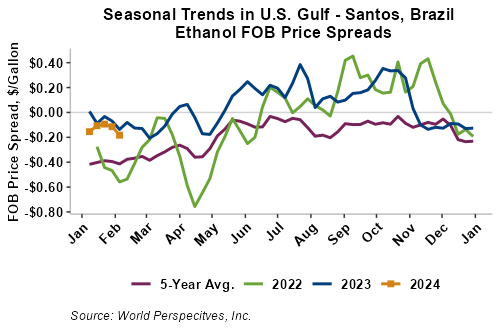

The FOB Gulf-Santos, Brazil ethanol spread has widened from last week’s close through Tuesday’s trading and is currently at -4.98 cents/liter (-18.84 cents/gallon).

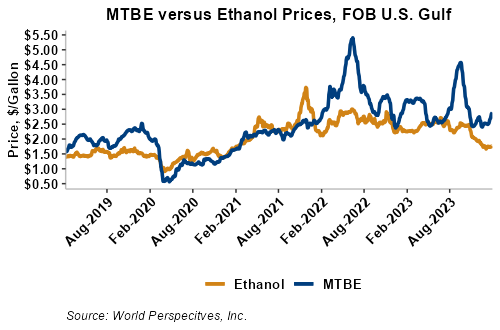

MTBE prices rose 7.1 percent last week and extended those gains in early week trading to gain 4 percent from Friday’s close through Tuesday’s trading. MTBE’s premium to FOB Houston ethanol has increased from last week’s report and stands at 29.51 cents/liter (111.71 cents/gallon).

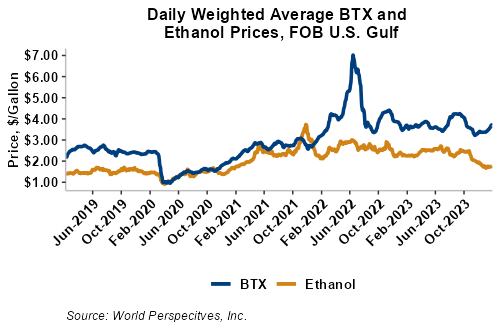

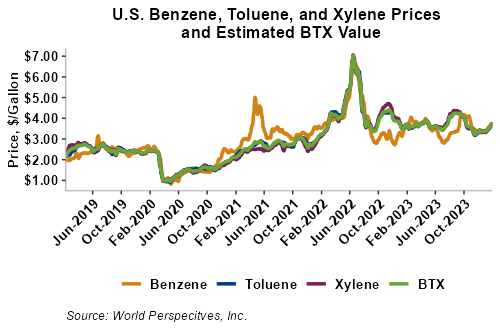

BTX component prices were sharply higher last week and continued that dynamic through Tuesday’s market close: Benzene was up 1.4 percent while Toluene was up 1 percent, and Xylene was up 1 percent. The estimated weighted average aromatic price is currently 97.89 cents/liter (370.56 cents/gallon), up from last Friday’s close. The BTX-Houston ethanol spread widened last week, and the weighted average BTX price is 51.25 cents/liter (193.99 cents/gallon) higher than the FOB Houston ethanol price.

Gasoline and petroleum products were higher last week but reversed course in early week trade. RBOB futures are down 1.5 percent to start the week while 84 octane RBOB (Houston) and 87 octane CBOB (U.S. Gulf) gasoline prices are down 1.8 and 2.9 percent, respectively. WTI futures are 0.3 percent lower at $77.8/barrel while Brent futures are down 0.5 percent to $82.5/barrel, from Friday through Tuesday’s close.

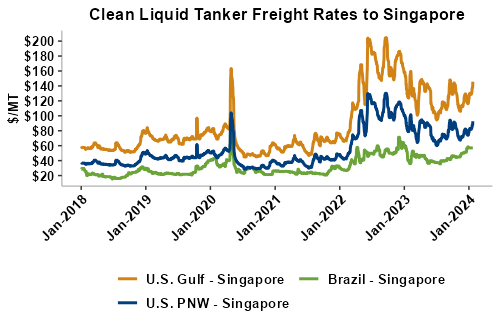

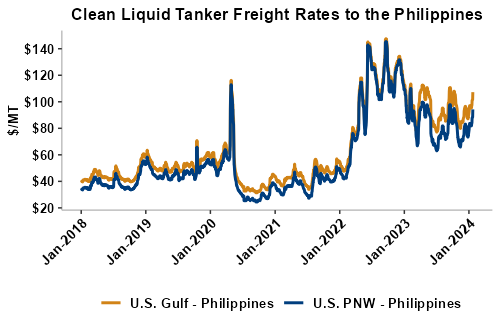

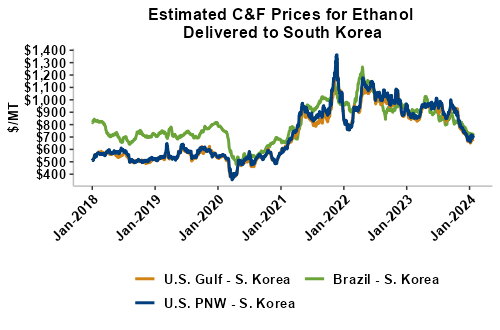

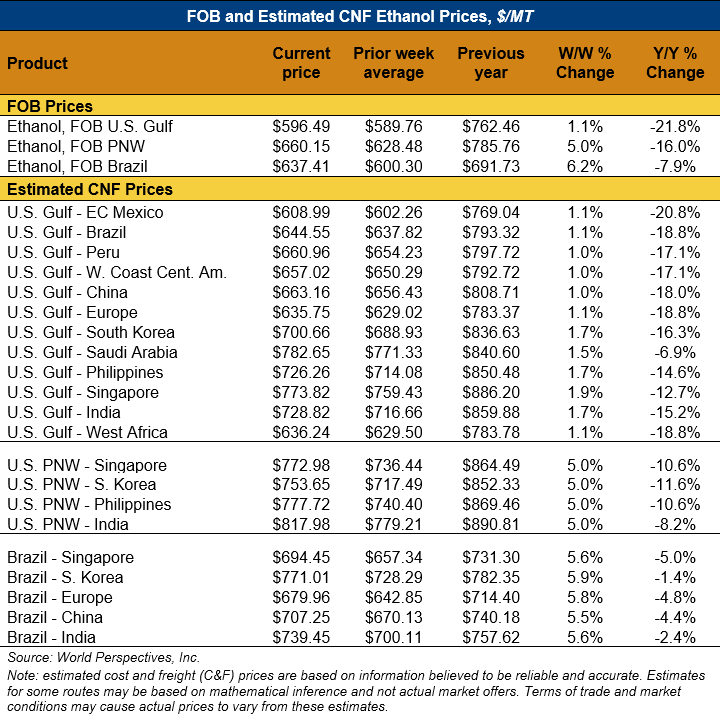

Liquid tanker rates are 2 percent higher on average this week with offers for the U.S. Gulf to South Korea seeing the largest gains (up 5 percent). Freight from the U.S. Gulf to the East Coast of Mexico saw the largest declines and is down 0.1 percent from last week. On average, tanker freight from the U.S. Gulf is up 2 percent this week while freight from the PNW has posted a 5 percent increase. Liquid tanker freight rates from Brazil are up 1 percent, on average, this week. Freight rates across all origins are 62 percent higher than this same week in 2023.

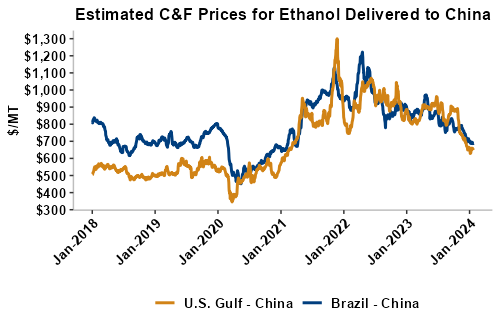

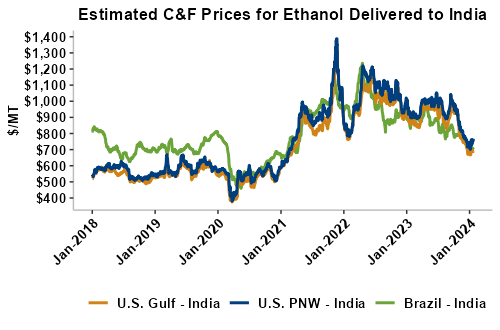

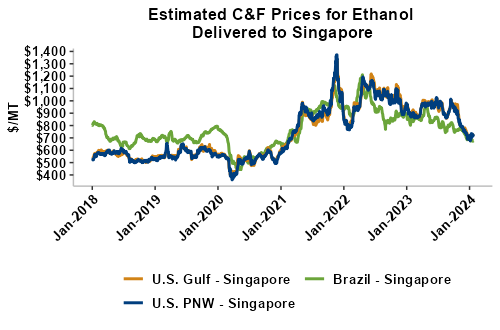

On a cost-and-freight (C&F) basis, offers are mostly higher this week as both freight rates and FOB ethanol offers have climbed higher. Prices for ethanol C&F to Central America from the U.S. Gulf are up 1.1 percent this week and are down 18.4 percent from this same week in 2023. Values for PNW ethanol to Southeast Asia average $768.12/MT this week, up 5 percent from the prior week but down 10.9 percent year-over-year. That compares to U.S. Gulf to Southeast Asia C&F prices that average $733.58/MT and are up 1.8 percent from last week but are down 14.5 percent year-over-year. C&F prices for Brazilian ethanol to Southeast Asia are up 5.7 percent from last week.