Ethanol Market Overview

- Brazil is the second largest producer and consumer of ethanol in the world and was the first country to implement a national fuel ethanol policy.

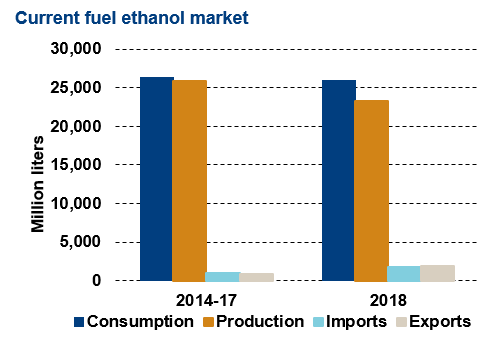

- In 2018 ethanol demand was 26 billion liters, 43% of the total gasoline market (including ethanol).

- Historically, Brazil was a net exporter supplying markets globally. In 2017, Brazil became a net importer due to feedstock economics from a tight sugar sweetener market. Brazilian sugarcane ethanol qualifies as an advanced biofuel in the U.S.

- Brazil also imports large volumes of ethanol, due to seasonality of sugar harvest and geographic distribution of feedstock production that is more accessible from the U.S., at a lower cost.

Key Facts

- Mandate:

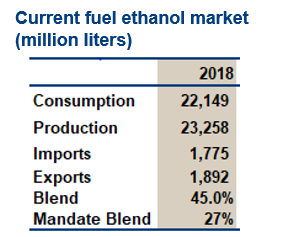

2018 27% - Ethanol consumption:

2018 26.0 bn liters (45% overall blend) - Capacity: 40.4 billion liters

- Ethanol plants: 390 (feedstock: sugarcane)

Policy

- Brazil has had a fuel ethanol policy in place since 1973 which included a blending mandate designed to support the domestic sugar industry. The percentage blend has varied since its initial introduction and is set within a range to allow for variation in the cane crop. Currently all gasoline must be blended with 27% ethanol. There is also a substantial market for E100, this is not mandated and depends on the price competitiveness of ethanol versus gasoline to the consumer. The availability of cheap fuel ethanol led to widespread sales of flex-fuel cars which can use any ratio of gasoline and ethanol, these cars now make up the majority of the vehicle fleet offering huge potential demand. This has linked ethanol prices to those of gasoline as consumers will switch freely between them, choosing the cheaper option at the pump.

- The gasoline price in Brazil has historically been set by the government in order to control inflation. However since October 2016, state oil company Petrobras has begun a new pricing policy to set domestic prices in line with world prices. This impacts ethanol thanks to the competition at the pump so higher gasoline prices translate directly into higher ethanol prices. The Brazilian government also supports ethanol through a number of fiscal measures. Federal taxes on gasoline are higher than those for ethanol, boosting the revenue of ethanol producers, in addition to this several states also have lower taxes for ethanol, increasing its competitiveness.

- As part of meeting its commitments to the Paris Agreement, Brazil is targeting GHG savings of 37% compared to 2005 by 2030. To aid this the government has announced an overhaul of biofuel policy through a new federal program called RenovaBio which is due to come into effect in 2020. The program will set emission reduction targets for fuel distributors which will require growing biofuel use. The system will be based on certificates issued by biofuel producers related to the GHG savings they provide which can then be traded. The government intends this policy to give more stability to the ethanol industry and has set an optimistic target for ethanol use at 40 billion liters in 2030.

Trade

- Brazil has historically been a net exporter and one of the main suppliers to the world market. In recent years, net exports have declined but it is still a significant exporter particularly to the United States, Korea, and Japan.

- The tight sweetener market in 2016/17 saw large scale imports entering the country, mainly from the U.S.

- In May 2017, Brazil’s Energy Ministry ruled that importers of ethanol must adhere to the same stock requirements as producers in an attempt to level the playing field. Mills are currently required to hold stocks equal to a minimum of 8% of their total anhydrous ethanol sales in the prior year by March 31st each year. This measure means that importers will need to invest in infrastructure and storage facilities to hold their stocks.

- On 1st September 2017, an import tariff on ethanol of 20% was implemented. The tariff is applied to imports above 150 million liters per quarter and will be in place for two years.

- In imported ethanol is further disadvantaged to domestic output as it does not qualify for tax exemptions.

Challenges

- If the government is to reach its target of increasing ethanol output and production, the program will need to provide sufficient incentives to encourage investment in mills and cane

- Many mills are experiencing financial difficulties and will need substantial support to grow. However, the recent poor economic conditions in the country mean that the government may struggle to afford the subsidies needed.

Market Outlook

- RenovaBio would generate the largest increase in demand for ethanol globally, demanding 14 billion additional liters of ethanol by 2030.

- Demand in Brazil will be driven by available supplies and sugarcane will continue to compete for the sweetener and ethanol market.

- Furthermore, six corn ethanol plants may come online in the near future.

- As fuel demand rises, the volume of discretionary use will fall, putting upward pressure on prices.