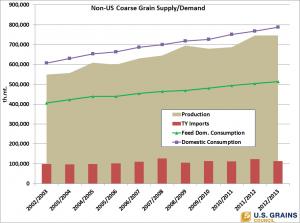

This week’s U.S. Grains Council’s Chart of the Week shows non-U.S. coarse grain production of corn, sorghum and barley over the past 10 years. In this time, production has grown almost 200 million metric tons or 36 percent, although 2012/2013 production is projected to be unchanged from last year due to disappointing harvests in other northern hemisphere countries (Europe, Russia and other Black Sea producers).

Non-U.S. coarse grain imports peaked in 2007/2008 at 126 million tons and then dropped 10 million tons the next year, spiking up to 124 million tons in 2011/2012. The U.S. Department of Agriculture projects that foreign imports will drop again next year.

Feed use outside the United States has climbed steadily, up by 26 percent or 107 million tons over the past decade. Likewise non-feed use grew steadily, up 37 percent or 73 million tons over the past 10 years.

In contrast, during the past decade the United States has experienced flat to declining coarse grain production since the peak in 2007/2008. Production in 2012 is estimated at 243 million tons down 30 percent from the peak. Feed use has declined steadily since 2004/2005, down from 163 million tons to 108 million tons in 2012/2013. At the same time non-feed use, driven by ethanol production, grew 90 million tons, from 64 million tons to 154 million tons.

While the U.S. share of world coarse grain imports has fallen over the past six years, a return to trend yields in 2013 will mean a bumper crop and opportunity for U.S. coarse grains to resume their leadership role in meeting the growing world demand.