The COVID-19 pandemic is changing the markets and our working situations on a day-to-day basis – but what is not changing is the U.S. Grains Council’s commitment to you, our members’ valued customers.

The Council’s staff worldwide are committed to providing you the service and market information you have come to expect from us during this time. While we are teleworking, we remain ready to assist you and encourage you to contact us as issues or questions arise.

The Council wishes all our customers around the world good health and safety during this trying time.

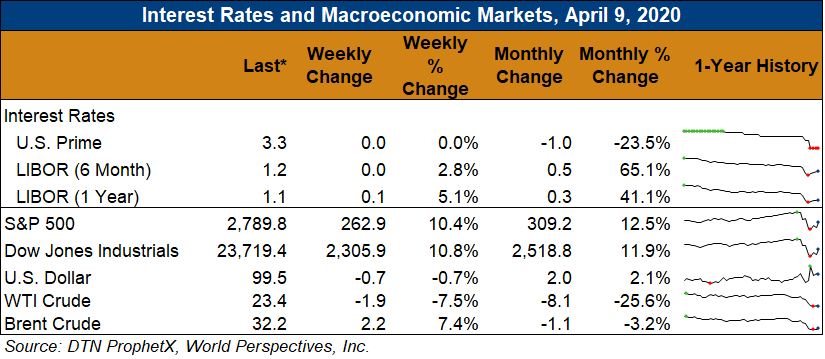

Chicago Board of Trade Market News

Outlook: May corn futures are 1 cent (0.6 percent) higher this week following a week of fund selling and commercial buying along with a neutral WASDE report on Thursday. Starting last week, funds were net sellers of corn futures and pushed the May contract to new lows on Monday, but commercial buying was aggressive on the dip and offered support to the market. Thursday’s WASDE report offered something for both bulls and bears but is viewed as neutral overall.

The headline WASDE figures for corn were a 5.08-MMT (200-million-bushel) increase in U.S. 2019/20 ending stocks and a 5.8 MMT increase in world ending stocks for the same year. The increase in U.S. carryout supplies was largely driven by a 9.07-MMT (355-milion-bushel) reduction in ethanol corn consumption. The USDA increased its expectation of feed demand, due to large hog and cattle inventories, by 3.8 MMT (150 million bushels), which helped offset the effects of the ethanol use reduction. Before the report, the market was expected a decrease in the U.S. export forecast, but USDA made no such changes, which was viewed as bullish. The final 2019/20 U.S. ending stocks figure was pegged at 53.14 MMT (2.092 billion bushels), leaving an ending stocks/use ratio of 15.1 percent. USDA lowered its average farm price by 20 cents/bushel due to the higher carry out level.

Internationally, USDA defied many expectations by leaving the Brazilian and Argentine corn crop estimates unchanged at 101 and 50 MMT, respectively. Brazil’s crop agency, CONAB, raised its expectation of the country’s corn crop to 101.9 MMT on Thursday, and many in the market expected USDA to offer a similar upward revision. USDA did, however, increase its forecast of 2019/20 EU corn production by 1.6 MMT. USDA increased global feed use by 3.5 MMT and increased global trade fractionally. USDA’s 2019/20 world ending stocks are estimated at 303.2 MMT, up 5.8 MMT from the March 2020 estimate and down 17.8 MMT from 2018/19.

Beyond corn, USDA offered some minor adjustments to the U.S. sorghum and barley balance sheets. The agency lowered its feed use estimate by 0.635 MMT (25 million bushels) and increased its export forecast by 1.27 MMT (50 million bushels). 2019/20 U.S. ending stocks were left unchanged, but the agency lowered the marketing-year average price 5 cents/bushel. USDA increased the 2019/20 barley export forecast by 22,000 MT (1 million bushels) and lowered the ending stocks figure by an equal amount, leaving the price forecast unchanged.

The weekly Export Sales report was bullish the corn market with 1.873 MMT of gross corn sales and 1.849 MMT of net sales reported this week. The net sales figure up sharply from the prior week as international buyers has become aggressive on the recent price break. The weekly export figure reached 1.29 MMT, up 3 percent from the prior week and a marketing year high. YTD exports now stand at 19.5 MMT, down 37 percent from a year ago while YTD bookings (exports plus unshipped sales) stand at 33.75 MMT, down 23 percent.

Cash corn values are steady across the U.S. this week with the average basis level dropping 1 cent to average 28 cents under May (-28K) futures this week. Farm sales have slowed on the recent break in futures prices, which has helped stabilize basis levels even as futures have moved lower. Barge CIF NOLA values are steady this week while FOB NOLA offers also unchanged amid a pickup in international demand.

Sorghum prices continue to grind higher, though this week’s price gains have been more moderate than the past two weeks. Japan and China continue to book sorghum sales and FOB NOLA export offers are 180 cents over May futures (180K) this week, up from 140K just three weeks ago. FOB Texas Gulf offers are 170K as of today’s market close, up over 30 cents/bushel from March offers.

From a technical standpoint, May corn futures have tested and rejected new contract lows and are moving sideways in a tight trading range. The new contract low ($3.25 ½) is now a major technical support point while the 10- and 20-day moving averages are technical resistance. Funds are starting to cover some of their short position amid the two-week increase in export sales and solid commercial buying. Seasonally, spring tends to see the development of weather scares that are often price supportive. The corn market is likely to trade sideways/higher for the foreseeable future.